Table of Contents

The failure of quantitative easing, both in the US under Obama and in Japan as Abenomics, is proof that the operations of banking cannot directly and immediately lead to economic growth, as explained by Adam Smith:

The judicious operations of banking can increase a industry, not by augmenting the country’s capital, but by rendering most of that capital productive.

This is opposite the notion of Keynes that interest rates, set by banks, are the key to growing an economy:

The interest rate policy of the central bank can alter the money supply. This makes it a real determinant of the economic scheme.

In fact, Keynes’ notion of interest rates is fundamentally opposite to those that came before:

| Author | Interest Rate is.. | Paradigm |

|---|---|---|

| Smith | ..the profits in lending | Classical |

| Ricardo | ..the reward in lending regulated by the rate of profit | Classical |

| Pigou | ..the reward of waiting for money to become capital | Classical |

| Marshall | ..the price paid for the use of capital | Marginalist |

| Mises-Hayek | ..the ratio between the difference in the price of consumer goods to capital goods | Libertarian |

| Keynes | ..the reward for letting go of cash | Neo-Classical |

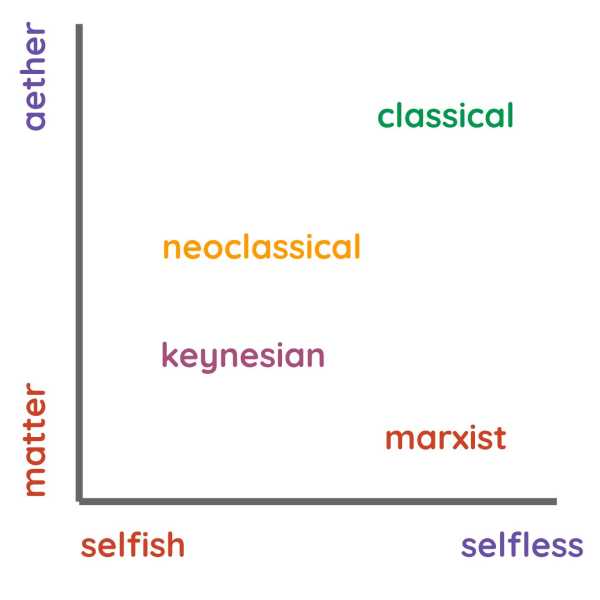

These differing definitions expose the different biases of the minds of their originators:

- The minds of Classical economists such as Smith, Ricardo, and Pigou viewed interest from the perspective of society. This led them into welfare economics. This appeals to compassionate minds.

- The mind of Marginalists, such as Marshall (and Samuelson), viewed interest from the perspective of the seller and buyer of capital. This is consistent with the equilibrium concept of the Marginal Revolution and Game Theory. This appeals to mathematical minds.

- The mind of Mises-Hayek view it from the perspective of an individual, either as a consumer or producer. This appeals to selfish minds who care only for themselves.

- The mind of Keynes views it from the perspective of a government or bank that serves all. This necessarily leads him to advocate deficit spending, open market operations which later became quantitative easing. This appeals to socialist minds or those that want everyone to follow them. The main difference between Keynes and Marx is their definition of value and money

From here, we can explain the affinities and oppositions of different beliefs and mindsets:

- Classical economics is the polar opposite of Marginalism which enshrines math and science. Xenophon and Smith have no equations at all, which makes them unacceptable as the basis of Economic ‘science’* which currently has econometrics, derivative equations, and stochastic calculus

- Keynesian economics** and Marxism are the opposite of the Austrian economics of Von Mises, Hayek, and Lbertarianism

*Superphysics understands all these definitions, but is based on Classical ones since it views the society as a metaphysical organism. The mathematical analyses will be done by machine learning. Economist will predictably say that Smith’s invisible hand is pseudo-science, and so we put Superphysics in its own field as Dialectics, which is above Science but under Metaphysics or Philosophy

Nov 2021

How did interest rates suddenly become so important to Economics?

From the era of Classical Economics of Xenophon and the early Marginal Revolution of Marshall up to Arthur Pigou (the ’last’ Classical economist) of the 1920s, money, banking, and interest rates were not so critical in Economics compared to how it is today.

In fact, Xenophon says that money can be banished and the economy would still work. This is supported by Adam Smith:Among the Mongols and shepherd nations who are ignorant of the use of money, cattle are the instruments of commerce and the measures of value. Wealth to them consisted in cattle, as to the Spaniards it consisted in gold and silver. Of the two, the Mongol notion was the nearest to the truth.

This is even supported by Ricardo:

The interest of money is not regulated by the rate at which the Bank will lend, whether it be whatever percent, but by the rate of profit which can be made by the employment of capital. This is totally independent of the quantity or of the value of money.

This is directly opposite the belief of Keynes who established the love of cash as being fundamental to Economics, as liquidity-preference:

The psychological time-preferences of an individual need two sets of decisions.

1. The time-preference which I call the “propensity to consume” – this determines for each individual how much of his income he will consume and save.

2. His liquidity preference – How long does he intend to have his money savings and not spend it?

The mistake of previous theories on the rate of interest is that they neglect the liquidity preference. This neglect is what we are repairing.

Instead of solving poverty*, inequality, recessions, bubbles, etc. by balancing productivity, Keynes’ solution was to use money – as money supply and banking. The stagflation of the 1970’s and the failure of quantitative easing after 2008 are double proofs that Keynes was wrong.

This was because Keynes shallowly believed that poverty and unemployment were caused by the thirst for cash.

- This was naturally quenched by banks.

- This then logically led to the dominance of interest rates.

- This leads to open market operations and quantitative easing.

*A proof of this is the current obsession by banks to ‘bank the unbanked’. This sophistry is just another way for bankers to find more customers and keep themselves employed, as opposed to letting those customers spend their savings themselves or move over into crypto (the competition of banks).

We can say that:

- Thomas Mun’s book, England’s Treasure on Foreign Trade, transferred economic power from monarchs onto merchants

- Keynes’ General Theory transferred economic power from merchants into merchant-banks which trade paper instruments on the ‘money market’, just as merchants traded commodities in the commodities market

These then make financial crises bigger than natural, as proven by the 1997 Asian Crisis and the 2008 Financial and Eurozone crisis.

Why did Keynes suddenly overturn tried and tested maxims on money from Ancient Greece and interest rates from Adam Smith?

An Effect of the Industrial Revolution

From the 1870’s to the 1920’s, there were huge improvements in technology as steel production, railroads, electrification, telecoms, flight, and mass production*.

*Outside of the West, Japan was the most successful in industrializing, being able to build their own battleships by the end of the 19th century. This explains why they were also the first to do quantitative easing.

These opened up massive investment opportunities which then required more banks and the rationalization of money. This led to:

- the consolidation of bimetallism into the gold standard

- the establishment of the Federal Reserve and giant banks like JP Morgan

- speculation opportunities that come with investments, manifesting as the Great Crash of 1929

Rather than bash speculation and profit maximization, Keynes overthrows Classical Economics in order to keep the growth going. His macroeconomics puts the governments in charge of the economy, through public debt. This is agreeable to the banking industry which gets employment from the circulation of cash, even if it leads to nothing productive. Examples are:

- wasteful government spending, such as Greece’s spending for the wasteful Athens Olympics

- universal basic income and conditional cash transfers like Bolsa Familia which do not translate to economic growth

Overthrowing Keynes’ Definitions

To solve stagnation, the correct solution is to break up capital which is amassed in paper assets such as a stock corporations, funds, and debt. The amassed capital is like pooled water that floods a certain sector, while causing a drought in the rest of the economy.

This can be done by bringing back the ideas of Classical Economics:

- restoring barter credits and real valuation, as valuation in wheat or rice, as described by Smith and actually used in the Inca and Khmer empires and ancient China as explained by Confucius.

- restoring the gold standard as bank gold which is a fixed quantity as opposed to commercial gold. In this way, governments will be less tempted to sell their gold reserves for fiat.

These offer competition against the fiat system without needing scam crypto.

- gold does not need electricity nor the internet but just needs security infrastracture as vaults which already exist

Instead of open market operations, the main tool for growing the economy will be allowing many new barter-credit banks, and import-export clearing banks to open, with smaller capital.

The money supply will be grown by multilateral clearing using national clearing funds pegged to the gold standard, as explained by economist EF Schumacher.

This is the opposite of the current system where banks merge and conslidate in order to have a bigger pool of fiat cash to lend.

In this Classical system, the credit worthiness of the borrower will be the main focus, instead of the interest rates since barter credits incur no interest as they are based on the value of wheat or rice which fluctuate.

Profit maximization is:

- checked by semi-state owned corporations which deal with utilities and public works as explained by Adam Smith in Book 5 of the Wealth of Nations.

- replaced by purchasing power as the net real value of barter credits and barter debits over time (how much value each person gets and gives now compared to his past self)

Leave a Comment

Thank you for your comment!

It will appear after review.